Have you heard the term Private Mortgage Insurance (PMI) when looking to finance real estate?

You may be wondering what PMI is and how you know when you need to purchase it.

These answers can be hard to find among all the real estate jargon you might be hearing lately.

Below is the short version of what you need to know.

What is Private Mortgage Insurance?

Private Mortgage Insurance is an insurance premium required by some lenders to offset the risk of a borrower defaulting on their home loan.

When you put down less than 20 percent of the real estate’s purchase price, the lender will generally require that PMI is added to the loan.

It is usually added into the monthly mortgage payment until the equity position in the real estate reaches 20 percent. However, there may be other options available in your area.

Under the current law, PMI will be canceled automatically when you reach 22 percent equity in your home, if you are current on your payments.

If you aren’t current, the lender may not be required to cancel the mortgage insurance because the loan is considered high-risk.

After getting caught up on your payments, the PMI will likely be cancelled. Any money that you have overpaid must be refunded to you within 45 days.

What if Your Real Estate Increases in Value?

With a conventional loan, it may take as many as 15 years of a 30-year loan to pay your balance down 20 percent making the minimum monthly payment.

But, if property values in your area rise, you might be able to cancel the PMI sooner.

Some lenders may be willing to consider the new value of your home to determine the equity in your home.

You may, however, be responsible for any fees, like an appraisal, that are incurred to assess the new value of your property.

In the end, private mortgage insurance is likely a good option if you can’t afford a down payment of 20 percent of the purchase price.

Now May Be A Very Good Time To Take Action

With all of the activity happening the housing market, now may be the best time for you to purchase your new home.

A smart next move would be speaking with a qualified home financing professional to learn which programs and down payment options are available in the Fremont area.

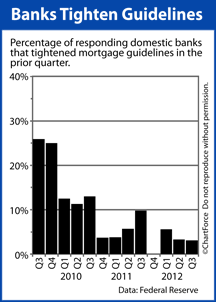

According to the Federal Reserve’s quarterly Senior Loan Officer Survey, it’s getting easier to get approved for a home loan.

According to the Federal Reserve’s quarterly Senior Loan Officer Survey, it’s getting easier to get approved for a home loan.